GBR

GBR A Strategic Analysis of the Vodafone Group

| ✓ Paper Type: Free Assignment | ✓ Study Level: University / Undergraduate |

| ✓ Wordcount: 4074 words | ✓ Published: 9th Dec 2020 |

Contents

- Introduction

- SWOT Analysis

- Telecommunication Industry: Current Market and Vodafone’s Position

- An analysis of the Key Metrics and Vodafone Valuation

- Share Price/Equity Value

- Cash/Cash Equivalents

- Cost of Global Expansion

- Trading Value

- Vodafone & Peer Financial Analysis and impact of Financial Policies

- Review of Vodafone Strategic Direction

- Rollout of 5G

- Digital Rebranding: Lead the Industry in the transition to Digital

- Cost savings through digital marketing

- Revenue boosting through digital marketing

- Global Brand Positioning

- Possible sale of assets

Introduction

Vodafone is a telecommunications company that operates in Europe, Africa, the Middle East, and Asia Pacific. Vodafone products include mobile services such as call, text and data, broadband, video content, mobile money, cloud security and hosting and, Internet of Things (IoT) services. Vodafone target customers include small and medium businesses, large corporates, multinational firms and public sector enterprises. Vodafone share price has fallen 37% since the start of the 2018, over 50% in less than five years and are now trading at the same level as almost a decade ago. On behalf of the equity research department here in Morgan Stanley I plan to critically carry out a Strategic Analysis of Vodafone. To do so, I have undertaken the following:

- Prepared SWOT Analysis

- Evaluated Telecommunications Market and Vodafone Position

- Review Vodafone and Peer Financial Analysis & Impact of financial policies.

- Highlight Key Competitive Advantages & Profit Drivers

- Review Vodafone Strategic Direction

SWOT Analysis

| Strengths | Weaknesses |

|

Wide range of services - Complete communications services including fixed broadband, video content, mobile, cloud and Internet of Things (IoT) business solutions. Industry leader in several markets - Ranks the largest/second largest mobile operator in the country in which its operating in terms of revenue market share. Brand strength raises the profile of group's distribution channels and drives purchasing decisions for customers. Robust geographic footprint - Leading international mobile telecom companies Largest mobile footprints, with over 290,000 mobile base station sites. (2017) |

Weak liquidity position - Liquidity position weakened which may limit its ability to fund potential opportunities arising in the market. Spain & Italy Market - Weakest markets in the past year include Italy and Spain. |

| Opportunities | Threats |

|

IoT market represents growth opportunity - The Internet of Things market has been growing at a CAGR of 13.1% since 2015 and is expected to continue at this rate until 2021. Strategic partnerships - Continues to strategically enter into global partnerships to expand its geographic presence and strengthen its offerings. Emerging Markets - Growing presence in emerging markets offers significant potential |

Growing competitive pressure could reduce market share and profitability - Competitive market with many alternative providers. Internet-based companies and software providers – new, strong competition. Had to decrease prices to remain competitive – further declines in future? Telecommunication Industry - Weak performing industry |

The SWOT analysis above helps to identify the areas in which further analysis of the company is required. This analysis will then identify the areas of risk to the company and the profit drivers of the business. The formation of a corporate strategy can then be shaped after such analysis has been completed.

Telecommunication Industry - Current Market and Vodafone's Position

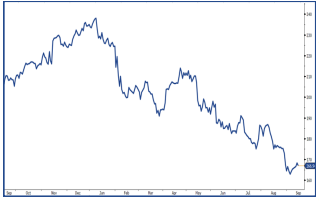

The telecoms market has been suffering in the previous two years as even the largest companies in the industry have struggled to attain any substantial amount of growth. In 2017 it was named one of the poorest performing sectors and least confident market for investors to have stakes in. The graph below provides us with a visual for the negative trend over the year 2018 in the FTSE Eurofirst 300 Telecoms index. The index declined by 18.6% in comparison with only a 9.3% drop in the broader FTSE Eurofirst 300 index. These statistics would be worrying for any shareholder and the trend does not show any sign of change.

Software companies such as Amazon or Apple, recently awarded the top brand names in the world, have taken over market share, meanwhile Vodafone’s brand value fell 14% along with other telecom companies. This is making it more difficult, in an already struggling industry, for Vodafone to maintain a competitive position. They have been forced to decrease prices to remain competitive in the industry and a possible further decline is predicted for the future. This expected fall in profits will have a negative impact on the equity value of the company.

An Analysis of the Key Metrics and Vodafone Valuation

Share Price/Equity Value

The graph above indicates that Vodafone share price has traded down recently. This is due to issues in the industry, emerging market exposure and the high CapEx spending that is required in the rollout of 5G.

Cash/Cash Equivalents

Key balance sheet metrics such as cash and cash equivalents have experienced a 31.6% decline from €12,922mn in 2016 to €8,835mn in 2017. A worrying figure in any analyst’s view as there is not enough cash equivalents to absorb the worsening net debt figure. The company added 128,000 fixed customers in the first quarter, a slower rate than in previous quarters, however this trend was seen across the telecom industry and is not specific to Vodafone operations.

If you need assistance with writing your assignment, our professional assignment writing service is here to help!

Assignment Writing ServiceCost of Global Expansion

Vodafone recently acquired Liberty Global’s Central and European cable networks for €18bn. This has transformed Vodafone, a mobile phone pioneer, into Europe’s largest broadband player. The company is continuing to secure new deals, including the recent acquisition of several 5G assets in Italy for the total sum of €2.4bn and is expanding into developing countries such as South Africa and India. The acquisition of Idea Cellular in India has allowed Vodafone to claim 35% of the market share, effectively making the company the industry leader in the country. The increase in the company’s global footprint is increasing its overall revenues but is also increasing their emerging market exposure. Emerging markets (EM) now represent a sizeable portion of their turnover. However, global concerns about EM is currently having a negative effect on the equity value of the company. This being said, continued success in these developing markets should eventually boost confidence and lead to an increase in share price in the long run.

Trading Value

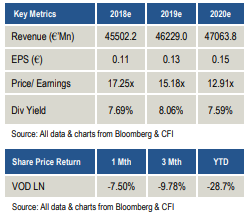

The Financial Times state that the company trades at 11 times earnings in comparison with an industry average of 15 times. This may be a sign of strategic drift and that the level of innovation in the company is slowing. The lower P/E also means that the company may be vulnerable to takeovers and management might need to start compiling a defensive strategy to ensure this doesn’t happen.

Vodafone & Peer Financial Analysis and Impact of Financial Policies

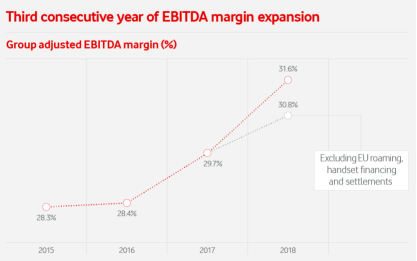

This graph presents three consecutive years of Vodafone EBITDA margin improvement at 30.8%. Guiding 1-5% underlying EBITDA growth and showing that relative to revenue, the company’s earnings are increasing. Operating efficiency is delivering faster EBITDA growth than revenues in 20 markets.

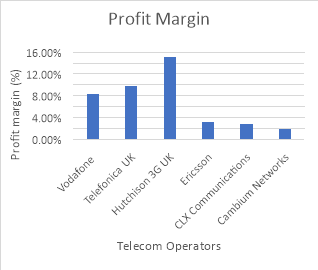

Vodafone’s total profits amount to £2,142mn which far exceeds that of its peers. Telefonica’s profits of £416mn is the second highest in terms of profit with Hutchinson below this figure again.

The company’s profit margin however, places it in the middle of the rankings amongst its peers with a profit margin of 8.33% in comparison to Telefonica with a profit margin of 9.76%. This suggests that the likes of Hutchinson and Telefonica might have a more efficient cost-based structures than the Group.

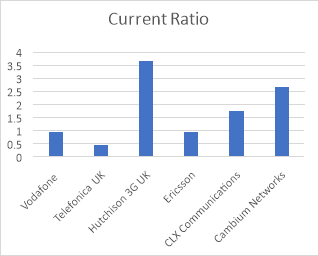

The company’s current ratio was 0.97 at the end of the year 2017, this figure was higher than Telefonica which had a CR of 0.45 but significantly lower than the current ratio of its competitor Hutchinson UK (3.68). A lower current ratio than the peers indicates weaker financial position of the company and creates uncertainty on its ability to meet short term obligations including dividends. (Source: https://fame-bvdinfo-com.ucc.idm.oclc.org/) The aggressive expansion outlined above in the previous section is not helping Vodafone’s net debt figure, which stood at €31.5bn at March’s year-end. That’s more than twice last year’s adjusted EBITDA. With currently dividend yield of 9% and forecast Dividend Yield at 7% to 8% as outlined in Table X below, many investment analysts do not believe that this dividend policy is sustainable.

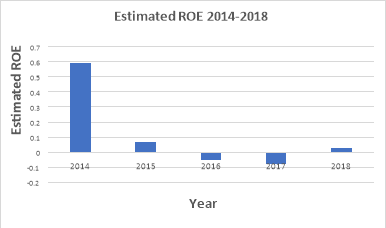

As an equity analyst it is crucial to evaluate the ROE of the company. As we can see from the graph above, the performance of the company has been falling since 2014. Currently at 2.7%, while up from last year’s -7.8% is not a strong indicator of performance. In comparison with the industry average of 13% it is worrying that management are not making efficient use out of the company’s equity. The high net debt figure on the balance sheet should, if anything, distort this figure upwards which is a worrying likelihood that this figure could be in fact lower that the figures above.

Our academic experts are ready and waiting to assist with any writing project you may have. From simple essay plans, through to full dissertations, you can guarantee we have a service perfectly matched to your needs.

View our servicesKey Competitive Advantages & Profit Drivers

Geographical Footprint

The company’s strongest competitive advantage is their wide geographical footprint with operations in over 26 countries and partners in more than 57 markets. The group is positioned in the industry as a global provider of telecom services whereas some of the largest telecom companies cater to single geography. This reduces business risks at a time when macro-economic conditions in Europe have been unfavourable and provides the company with incremental avenues for growth. It has done so through strategic acquisitions of stakes in various companies and partner networks across the globe. In 2017, approx. 72.5% of its revenue was accumulated from Europe and 24.6% from Africa, Middle East and Asia Pacific. One of its more recent mergers with Liberty Globals’s German and eastern European cable networks (€18bn) is expected to be a source of catalyst looking forward and is said to be Vodafone’s biggest push into broadband.

Leadership Position in Broadband

The company provides a wide portfolio of services including a large presence in broadband services. Vodafone has held the title of Europe’s fastest growing and leading challenger in broadband, adding 1.1mn households and 0.8 million converged customers last year, reducing attrition rate and increasing average revenue per customer.

Internet of Things Division

Vodafone has remained the industry leader as the business continued to outperform peers in the telecom industry, despite an overall declining market environment. This is attributed to the success of their Internet of Things (IoT) division, which according to industry estimates, is expected grow strongly in the coming years. This is predicted to become a profitable division within Vodafone in the near future. The aforementioned factors are considered the competitive advantages of the firm and will be the factors that drive the growth, on condition that the company’s corporate strategy plays to these strengths. The equity value of the firm may be moving in a negative direction currently but if management act soon and act correctly, they have to power to turn things around in the medium-long run.

Review of Vodafone's Strategic Direction

Vodafone Group has a clear strategic direction under their new CEO, Nicholas Reads:

- Continue to focus on organic performance.

- Use Digital Vodafone to enhance the customer experience, while simplifying and streamlining their own internal processes.

- Achieve a higher level of efficiency and generate more returns.

It plans to deliver on these strategies by carrying out the following:

Rollout of 5G

The company is competing with EE and O2 to take a lead on the roll out of 5G networks in Britain. The company has claimed it will have 1,000 5G sites by 2020 including sites in more rural areas. The implementation of 5G will boost profitability by decreasing the costs of delivering one gigabit of data by approx. 70%. It will also allow Vodafone to sell modified services and deliver faster network speeds to consumers willing to pay more. “Vodafone has a history of firsts in UK telecoms - we made the nation’s first mobile phone call, sent the first text and now we’ve conducted the UK’s first holographic call using 5G.” - Nick Jeffery, Vodafone UK CEO. (Financial Times)

Digital Rebranding - Leading the Industry in the Transition to Digital

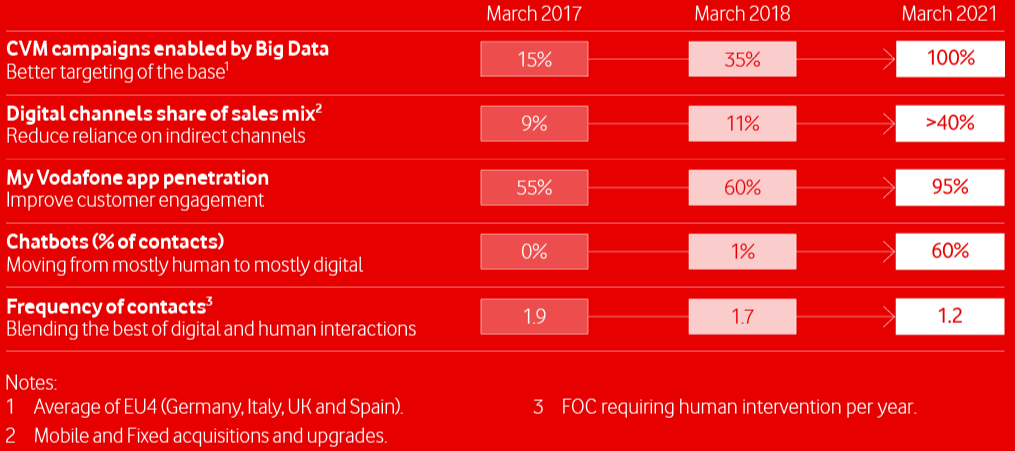

Maintaining a sustainable position in the market is becoming harder in today’s technologically advancing world. Staying relevant in the face of societal change remains a challenge for all industries including the telecommunication industry. There are a multitude of drivers constantly reshaping how business is conducted, in particular, new technologies. Vodafone has set upon digital transformation in order to remain competitive in their industry. A survey carried out by Euromonitor concluded that one of the most important aspects of a company’s value proposition is having a digital presence in the market. Vodafone have been said to be investing heavily into this are, supposedly aiming to reduce costs by €8bn by introducing robot machines that can replace more expensive labour. The group are implementing a new strategic development called “Digital Vodafone” to enhance customers’ experience. They will be able to satisfy any customer request through automated, digital support and increase the use of data analytics to provide predictive, proactive offers to their customers, making each user’s experience more personalised. The company sees substantial scope for digitalisation to accelerate the simplification and automation of standard processes, in both operational and support areas. Such areas include IT & network operations and other administrative activities. The table below outlines Vodafone’s medium-term goals.

Cost Savings through Digital Marketing

The company improved their cost base structure by lowering net operating costs on an organic basis for the second year in a row in 2017 and their ambition is to continue this trend over the long-term through the “Digital Vodafone” programme. By the 2021 financial year, Vodafone’s target is that over 40% of sales will be via digital channels, up from just 11% today. The company plans to make cost savings of €8 bn by digitalising key aspects in their customer management, technology management and operational processes, meaning many back-office functions will be taken over by “robots”, reducing the company’s labour costs. The new CEO plans on cutting 1,700 jobs across shared service centres in Egypt, India and Romania this financial year, roughly 8% of the workforce in that side of the business. This will allow them to reduce the commissions paid to third-party distributors and optimise the size of their retail footprint.

Revenue Boosting through Digital Marketing

The company is introducing new “smart capex” allocation methodologies, based comprehensive data analytics which will enable them to understand their profitability both by customer and by mobile site. Their investment in Digital Vodafone will strengthen their ability to market directly to their customers via the internet and the My Vodafone app. The impact of this new strategy will have a substantial effect on profits by 2021 and will hopefully provide the company with the extra revenue it needs to offset against its debt figures.

Global Brand Positioning

Telecom companies are striving to reach new audiences and gauge a wider share of the markets by creating a successful brand power. Vodafone’s efforts in launching a new sub-brand Voxi, aimed at reaching younger users, failed to take off, however, the Voxi move is part of a wider strategy to revamp its branding strategy as the telecoms market heads toward 5G. ‘The future is exciting. Ready?’ Is the new brand logo that has been selected in order to get across Vodafone’s futuristic views of the industry. Serpil Timuray, Vodafone’s Chief Commercial Operations and Strategy Officer and her team conducted research covering 32,000 people in 17 countries to tailor the company’s new “global approach”. Allowing Vodafone to collect relevant talent for adverts in each local market and then combine all the essentials into its global strategy. If this new branding strategy is a success it should fall into effect in medium term profits and in turn, the equity value of the company.

Possible Sale of Assets

Mr. Read, has raised concerns over the company’s debt profile and the sustainability of its dividend payments in the wake of its recent €18bn takeover. He believes that improving earnings performance along with asset sales would help reduce these borrowings In order to reduce the company’s debt pile of €31bn, the company is considering a sale of tens of thousands of mobile masts, on condition that the right deal presents itself. Barclays has estimated that €12bn stems to be made from such a sale. Mr Read is currently looking at how to balance Vodafone’s strategic network needs against the efficiency gains of offloading its masts on to a specialist company. He argued that there has been movement in the tower industry where independent groups or private equity-backed specialists have struck similar deals with struggling telecom groups. It’s not good enough to have a strategic plan in place. The strategy could be well aligned but if not articulated and realised, it will not have any beneficial impact on the company’s equity value. Recently appointed CEO, Mr. Deeds has his work cut out for him over the next few years but if implemented in the most efficient manner, the company’s corporate strategy might save the company just yet.

Investment Conclusions

There are some reasons to be optimistic about the future of Vodafone and its share price. These include:

- Broad Geographical footprint.

- Diverse range of telecommunications services.

- Significant brand awareness

- Increased focus on digital, cloud services, Internet of Things, 5G etc

- Cost saving opportunities through acquisition synergies and focus on digital

All of the above can drive share price growth over time with a successful execution of its strategy as outlined above. However, in the short term there is significant down-side to the share price, to the unsustainable nature of the dividend yield at 9% and dividend cover of just 0.7. The company will need to increase revenue and EBITDA dramatically to maintain this. But forecasts show that EPS is expected to fall 12% in the year to 31 March 2019. They are then forecasted to grow 14% in the following year but that may not be enough. By this stage EPS will stand at 10.4p against a dividend per share forecast of 13.9p. Management may have to make a drastic change to the divided policy soon which might knock shareholders confidence in the company, causing the share price to fall further. Alternatively, an aggressive disposal strategy of non-core assets to reduce the debt burden may be the only alternative.

References

- EBSCO http://web.b.ebscohost.com.ucc.idm.oclc.org/ehost/pdfviewer/pdfviewer?vid=0&sid=9d9eb0f4-ce11-4975-b2fc-9cf98630fb0b%40sessionmgr120

- http://www.portal.euromonitor.com.ucc.idm.oclc.org/portal/Analysis/Tab

- Yahoo Finance (2018) These 2 FTSE 100 dividend stocks yield 9%, but is this mighty income sustainable? (online) Accessed on 10/11/2018 https://uk.finance.yahoo.com/news/2-ftse-100-dividend-stocks-162422608.html?.tsrc=applewf&guccounter=1

- http://web.b.ebscohost.com.ucc.idm.oclc.org/ehost/pdfviewer/pdfviewer?vid=1&sid=2cdf1937-f2c7-4b3c-930b-b4001d682988%40sessionmgr104

- file:///C:/Users/Sinead/Downloads/Weekly-Trader-17.09.2018.pdf

- https://www.vodafone.com/content/annualreport/annual_report18/index.html#financial-performance

- https://www.ft.com/content/1a072f38-8fd5-11e8-b639-7680cedcc421?kbc=cab4b7dc-d177-4173-8afc-21da673e2369

- https://uk.finance.yahoo.com/news/2-ftse-100-dividend-stocks-162422608.html?.tsrc=applewf&guccounter=1

- https://www.vodafone.com/content/annualreport/annual_report18/index.html#financial-performance

- https://www.macrotrends.net/stocks/charts/VOD/vodafone-group/roe https://markets.ft.com/data/equities/tearsheet/financials?s=VOD:LSE

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

DMCA / Removal Request

If you are the original writer of this assignment and no longer wish to have your work published on UKEssays.com then please: